This week marked the final monetary policy meetings of the year for major central banks, including the Federal Reserve (FOMC), the Bank of England (MPC), and the European Central Bank (ECB). Federal Reserve Chairman Jerome Powell’s surprising comments about initiating rate cuts and FOMC members’ interest rate projections indicating a 75 basis point cut for next year created a significant impact. While this aligned with market expectations for an early rate cut, a contrasting stance was reaffirmed by the ECB and the Monetary Policy Committee (MPC) of the Bank of England (BoE), which deemed it premature to discuss rate cuts. This dichotomy in policy directions has led to a weakening of the U.S. dollar.

The remaining central bank event for the year is the Bank of Japan’s policy meeting on December 19th. Bank of Japan Governor Haruhiko Kuroda’s cryptic statement about facing challenges at the year-end and into the next year heightened speculation about an early end to negative interest rates. Although subsequent reports denied the possibility of an immediate end to negative rates, the lingering perception of a narrowing interest rate gap between Japan and the U.S., following the Fed’s dovish shift mentioned earlier, remains strong. The USD/JPY pair has experienced volatility but is currently exploring lower levels.

However, regardless of speculations, absolute interest rate differentials between the U.S. and Japan or the U.S. and Europe can still incentivize carry trades. This week’s fluctuation in the yen market likely led to a reduction in speculative short yen positions. Investors seeking to pick up yen crosses at lower levels may find opportunities. On the other hand, if the Bank of Japan hints at an early exit strategy next week, it could reignite yen buying and lead to a correction towards yen strength. The outcome of the Bank of Japan meeting is uncertain, especially considering it falls in the week before Christmas, potentially adding further market unpredictability.

Looking ahead in the foreign markets, economic data releases include Canada’s housing starts for November, international securities transactions for October, and wholesale sales for October. In the U.S., the New York Fed Manufacturing Business Conditions Index for December, industrial production for November, and net long-term TIC flows for October are expected.

Regarding speeches by central bank officials, several ECB officials are scheduled to speak following the ECB meeting. These include Robert Holzmann, Governor of the Austrian National Bank, and Mario Centeno, Governor of the Bank of Portugal. Additionally, speeches from central bank officials from Slovenia, Estonia, Lithuania, and Croatia are on the calendar. From the Bank of England, speeches by Dave Ramsden, Deputy Governor for Markets and Banking, and Tiff Macklem, Governor of the Bank of Canada, are anticipated.

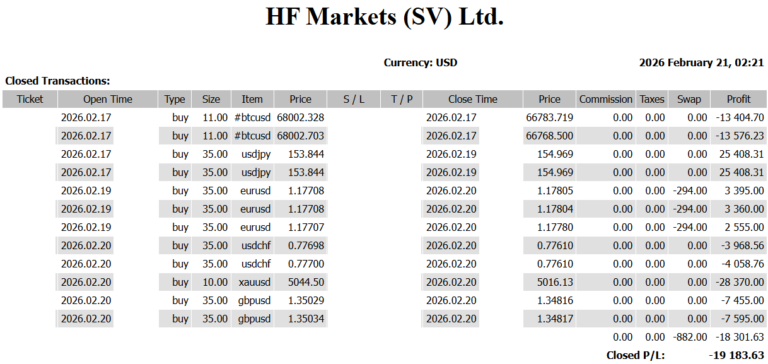

Today we will focus on the US PMI numbers. Once good numbers come out, USD will be bought back, but it is assumed that this will not last long and there will be selling. If this develops, we plan to sell USD.